In investing circles, it is a broadly accepted rule that property, that is houses, provides a great hedge against inflation. Simply, this means that property is great at protecting your money and its purchasing power from the damaging and erosive effects of inflation. In some ways, this is due to property being a tangible or a ‘real’ asset. Something you can touch and feel, as opposed to a dilutable share in a company.

With inflation in the UK set to hit levels not seen in nearly 30 years, can landlords put their feet up and lay back, protected from the inflationary storm? Unfortunately, the answer is not simply yes or no, rather a more convoluted ‘maybe’.

Can Property Investments Protect Against Inflation?

Over the last few decades, numerous studies have suggested that UK and US property markets can provide investors, landlords, and homeowners with natural protection against inflation. It is generally thought that as inflation increases, so do property prices.

However, it is not the case that simply by owning property, landlords in the UK will be protected from the most recent wave of inflation. The Man Group, the world’s largest publicly traded hedge fund, conducted a study into the performance of house prices in the UK during times of inflation. The results of the study suggest that simply owning property does not guarantee protection from inflationary pressures. Whilst property has consistently generated positive real returns in the long-run, short-term performance is less predictable. What is more, the performance of property during times of inflation depends upon both the type of inflation and more granular geographic performance.

Different Types of Inflation and Property Prices

The Man Group’s recent study found a clear distinction between periods of controlled inflation and periods of hyperinflation. During periods of controlled inflation, prices can increase due to long bouts of healthy economic growth. In these cases, property tends to outperform inflation and act as strong protection against inflationary pressures. In contrast, periods of hyperinflation occur when the economy overheats, with inflation and interest rates spiking in response. In these cases, the returns of most assets (property and financial investments) suffer, with property investors seeing the real asset values of their investments decline as house prices tumble or fail to keep pace with inflation.

What Type of Inflation are we Currently Experiencing in the UK?

As the saying goes, if you ask one hundred economists a question, you will get one hundred different answers. With that in mind, it is hard to say exactly what type of inflation we are currently experiencing in the UK. On the one hand, the spike in inflation is caused by external supply issues, such as logistical trade problems with Asia and a spike in energy prices due to the conflict in Ukraine and subsequent tensions with Russia. On the other hand, inflation is not yet high enough to really be considered anywhere near hyperinflationary, with the Bank of England describing the current high rates as ‘transitory’. In truth, it seems we are somewhere in between the two.

How Inflation has Historically Affected Property Prices

That being said, with oil currently over $100 per barrel, it is worth contrasting the current climate with that of the 1973 Oil Crisis. Similarly, to what we are beginning to experience, the 1973 Oil Crisis brought about significant inflation and tightening costs of living conditions for many in the UK. On the face of it, house prices continued to rise throughout the 1970s despite the 1973 Oil Crisis. Although, prices visibly stalled throughout the crisis. Even after OPEC lifted the oil embargo in 1974, house price growth continued at a slower rate than prior to the crisis. More interestingly, when inflation was brought into the equation, house prices actually fell in real terms throughout much of the mid-1970s. That is, although nominal house prices increased, they failed to keep up with inflation, and houses effectively lost value over the period. However, it is unlikely that the current economic and political climate will be anywhere near as disruptive as the 1973 Oil Crisis.

The UK Is Not One Single Housing Market

Whilst it makes life simpler to refer to it as such, it is an error to view the UK as one single identical housing market. The UK is in fact made up of hundreds of regional housing markets, each with its own dynamics and economic drivers. As such, different areas of the housing market respond in different ways to economic events and shocks. By way of example, during one of the most recent inflationary periods between December 2009 and September 2011, most house prices across the UK as a whole fell significantly, however prices in London rose by over 3.5% in the same period.

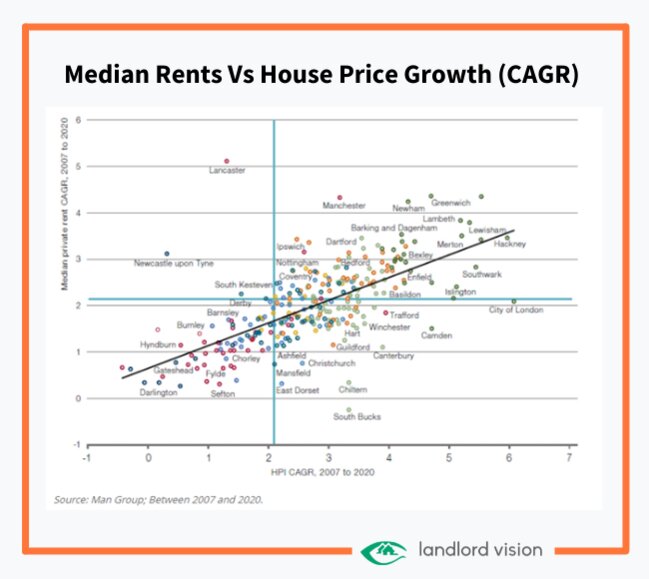

The Man Group has analysed the performance of property, both in terms of house prices and rent, over a number of years. They then contrasted the performance against average inflation since 2007 (indicated by the horizontal and vertical blue lines in the figure below). As can be seen, there is a huge divergence in performance between different locations. Unsurprisingly, areas like Manchester, Greenwich, and Lambeth have generated inflation-beating performance, both in terms of rent and in terms of house price growth.

More interestingly, there are a significant number of locations where the relationship between house price growth and rental growth appears to have broken down. Take, for example, the housing markets of Guildford, Canterbury, and Winchester, all of which have seen house price growth significantly outstrip inflation. Yet, whilst house prices rose sharply, rents remained suppressed and failed to keep up with inflation. At the other end of the scale, markets like Newcastle, Lancaster, and Derby all saw rents increase well beyond the rate of inflation, yet house prices failed to keep up.

Median Rents Vs House Price Growth (CAGR)

What Does Inflation Mean for Landlords?

If you were to close your eyes, throw a dart at the map and purchase a property in the location on which it lands, the odds are that your investment would just about beat inflation and protect the purchasing power of your capital. However, there is also a sizeable risk that your investment would fail to keep pace with inflation and lose value in real terms. In short, there is no guarantee that all property investment can act as effective protection against inflation.

Understanding the Diverse Property Market can be More Helpful When Hedging Against Inflation

That being said, on the whole, depending on the type of inflation, landlords should be able to weather the storm of inflation reasonably well. However, those seeking to thrive rather than just survive need to consider property on a more granular level. Whilst the UK property market as a whole may rise or fall, it is possible to outperform the market by assessing the specific dynamics of different local housing markets and seeking out the areas and properties with the most opportunity.

“What we need is a more targeted approach to property investment, looking to deliver returns that are robust even in periods of inflation. This requires a granular and differentiated strategy that takes into account geography, type of tenure and economic backdrop. Not all property investment is the same and we believe that, if we are entering a period of higher inflation, investors in property will need to respond to this by being more discerning as to how and where they deploy capital.”

Shamez Alibhai, The Man Group

Despite frothy house prices, increasing inflation, and the spectre of rising interest rates, there still remains an opportunity for landlords and investors to generate significant returns in the housing market by taking advantage of idiosyncratic opportunities and by spreading their geographic net to include areas with greater upside. The Man Group suggests that well-built houses in good locations, offering a range of tenures will continue to consistently outperform the broader market, irrespective of inflation.

References

Pettinger, T., 2017. The Economy of the 1970s. [Online]

Available at: https://econ.economicshelp.org/2010/02/economy-of-1970s.html#:~:text=The%201970s%20was%20a%20period%20of%20rapid%20house,In%201970%20Q1%2C%20average%20house%20prices%20were%20%C2%A34%2C377?msclkid=29a6106ca89411ecbd93c91177f1edfe

Sants, A., 2022. Russian oil embargo won’t be as damaging as 1973 oil crisis. [Online]

Available at: https://www.investorschronicle.co.uk/news/2022/03/10/russian-oil-embargo-won-t-be-as-damaging-as-1973-oil-crisis/?msclkid=14d7bd68a89b11ecad778052a0ed3ebe

The Man Group, 2021. Does property create a viable inflation-linked investment opportunity?. [Online]

Available at: https://www.man.com/maninstitute/property-as-an-inflation-hedge?msclkid=cf2600d9a86711ec9cf503429a2ba3e1

Disclaimer: This Landlord Vision blog post is produced for general guidance only, and professional advice should be sought before any decision is made. Nothing in this post should be construed as the giving of advice. Individual circumstances can vary and therefore no responsibility can be accepted by the contributors or the publisher, Landlord Vision Ltd, for any action taken, or any decision made to refrain from action, by any readers of this post. All rights reserved. No part of this post may be reproduced or transmitted in any form or by any means. To the fullest extent permitted by law, the contributors and Landlord Vision do not accept liability for any direct, indirect, special, consequential or other losses or damages of whatsoever kind arising from using this post.