The outlook for UK house prices is looking increasingly bleak.

The Bank of England has been caught off-guard by inflation, which is proving stickier than they initially expected. Consumer price inflation and employee wage inflation have both come in ahead of expectations recently, and as such, the BoE is going to have to respond to bring inflation back under control. Markets are now pricing in the prospect of interest rates rising beyond 6.5% before the end of the year, with analysts at JP Morgan suggesting rates could rise as high as 7%. Mortgage rates have since spiked as lenders price in the risk of rising interest rates, increasing borrowing costs for homebuyers and investors alike.

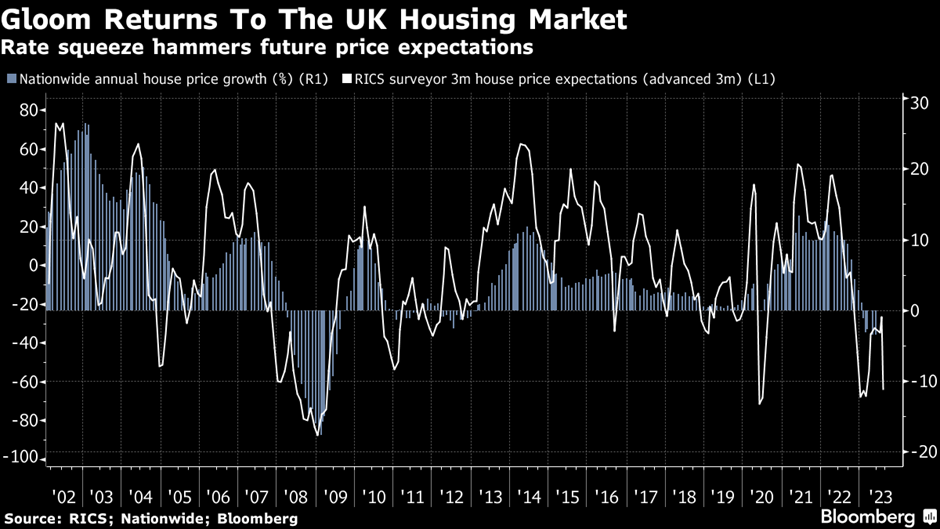

House Prices and Interest Rates are Often Linked

Typically, house prices have an inverse relationship with interest rates. The higher rates go, the worse house prices perform. Rising interest rates push up mortgage rates, increasing the cost of finance on a new property and reducing the amount people are able to pay. Therefore, reducing the upward pressure on house prices and increasing the likelihood of them falling. So, we should expect house prices to fall in the near future.

The challenge that many investors and commentators face is that most house price data is backward looking. It reflects homes which were purchased months ago and does not provide an indication of what is happening to house prices right now. This is why you may see recent headlines about house prices rising, at a time when rates are rising and the economic consensus suggests that they should be falling. So instead, it is better to take a look at ‘softer’, forward-looking sentiment-based surveys, such as the UK Residential Market Survey carried out by the Royal Institution of Chartered Surveyors (RICS). Their survey collates feedback and views of RICS members – surveyors and estate agents – to provide what Goldman Sachs deems to be ‘the best short-term lead indicator of house prices and activity’.

How Does the UK Residential Market Survey Work?

The survey expresses the responses as a number between positive 100 and negative 100, with positive 100 suggesting that every respondent believes house prices will go up and negative 100 indicating that every respondent believes house prices will go down. The latest June survey by RICS demonstrates that house prices are facing renewed downward pressures. New buyer enquiries and agreed sales are showing signs of slipping deeper into negative territory whilst sales expectations have continued to fall. Feedback from respondents highlights that house price sentiment has fallen dramatically, falling from a net balance of -30% in May to -46% in June. At the same time, 3-month house price expectations have dropped, with a net balance of -49% of respondents expecting them to fall, compared to -3% in May. This is especially worrying as typically the RICS price expectations survey has been a great indicator of future price performance, as John Stipek from Bloomberg highlighted in the chart below:

The chart compares the Nationwide House Price Index against 3-month house price expectations by RICS surveyors. As you can see, there is a strong correlation between the 3-month house price expectations and actual house price performance, indicating a sharp slide in house prices in the coming months. The question is, if house prices do continue to falter, by how much will they fall?

How Much Will House Prices Fall by?

The housing market tends to operate in quite predictable cycles, as highlighted by Fred Harrison’s theory of the 18 Year Cycle. As house prices rise, buyer sentiment increases in step further fuelling house prices to continue their rise. Vice versa, if house prices are falling, buyers become increasingly cautious and hold-off buying, which acts as a further drag on house prices. With this in mind, any continued weakness in house prices could well run-off into a prolonged period of declining prices. Many commentators are now predicting further prices falls by as much as 10-25%, depending on who you subscribe to. Not only that, but many predictions relate to nominal house price changes, that is the headline price of your house falling from £100,000 to £85,000 for example. If inflation remains persistent, the real value of houses may fall by an even greater amount.

Fundamentally, something has to give. Robert Gardner, chief economist of Nationwide, highlights that mortgage payments as a share of take-home pay are well above historical average, with prospective buyers finding it increasingly difficult to save for a new home.

Despite the higher interest rates available to savers, the sharp rise in rents together with continued high rates of inflation more generally, is continuing to make it difficult for many prospective buyers to save for a deposit.

Yet, predictions are just that, predictions, and there are examples of anomalies where RICS sentiment has been either overly exuberant or overly negative and house prices have failed to match expectations. It could well be that house prices defy expectations and remain more resilient than many would expect. Equally, inflation may prove to be less sticky than it initially appears, allowing rates to fall back to a more tolerable level. There is also the political aspect to consider, falling house prices never look good heading into an election, so it would not be out of the question to see a raft of government legislation introduced to support house prices in the short term.

What Does This Mean for Landlords?

Perhaps now more than ever, it is a time for landlords to be cautious. As a group, landlords do not benefit like homebuyers do, of being able to reside in their properties. Purchasing a property is an entirely financial enterprise for landlords, so it is important to ensure that you maximise your returns and avoid costly mistakes. With that in mind, although there is no guarantee that UK house prices will fall, the balance of probability certainly suggests that they will. Buying a house at the moment is like catching a falling knife, you may well be dexterous enough to do so, but it is highly likely that you will cut yourself in the process. The best bet may well be to wait until prices have settled.

Despite a turbulent forecast for house prices in the near future, landlords would do well to heed the words of Rudyard Kipling and treat triumph and disaster much the same. Beyond the immediate future, falling house prices could offer a once in a generational opportunity for investors to purchase properties at attractive valuations. Despite rising rents, net yields for many landlords are razor thin as mortgage payments eat into any profit. As house prices begin to fall, more and more profitable opportunities will begin to come to the market.

Not only do falling house prices afford investors a potential future opportunity, but the saying still rings true; ‘buy land, they’re not making it anymore’. In the long-term house prices have a habit of rising. Since 1992, house prices have generated a compound annual growth rate (CAGR) of 5.71%. For property investors who have added rental income or the use of leverage into the mix, their returns have been even higher. If your horizons are long enough and you are looking at property as an investment for the next 20-30 years, then a 5-10% decline in house prices right now is a mere blip on the graph and should be treated as such. Even the 20% fall experienced following the financial crash in 2008, looks insignificant when viewed in the context of the last 30 years.